Viraj Patel

@VPatelFX

FX & Global Macro Strategist by day | 90s R&B & Hip-Hop DJ by night | Views here are my own | @VandaResearch

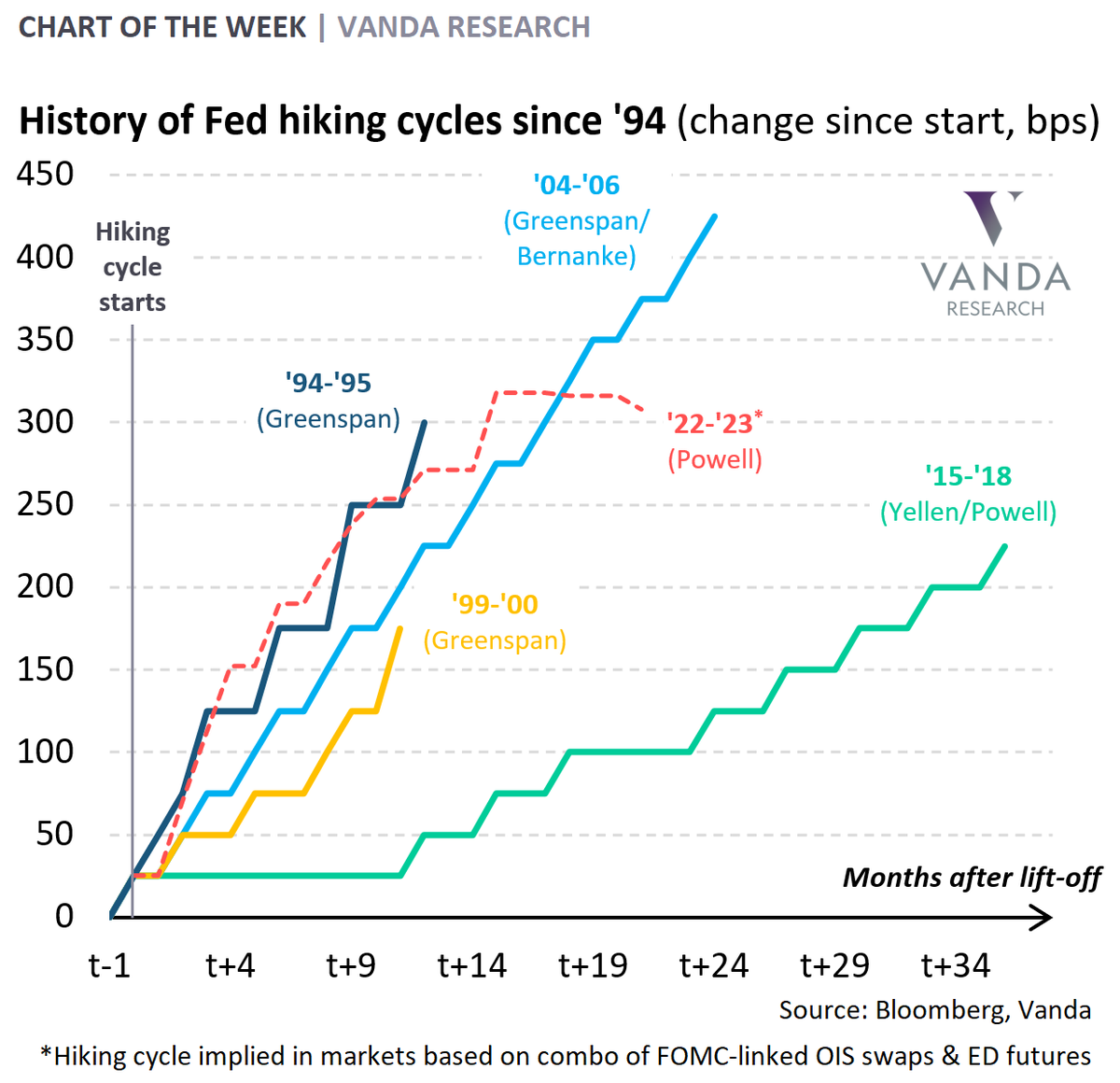

⚠️ Markets are pricing in the most aggressive front-loaded Fed hiking cycle in modern history. If the Fed delivers 4 consecutive 50bps hikes starting in May... which is starting to get priced in... then this will be more aggressive than what we saw in '94. History being made $USD

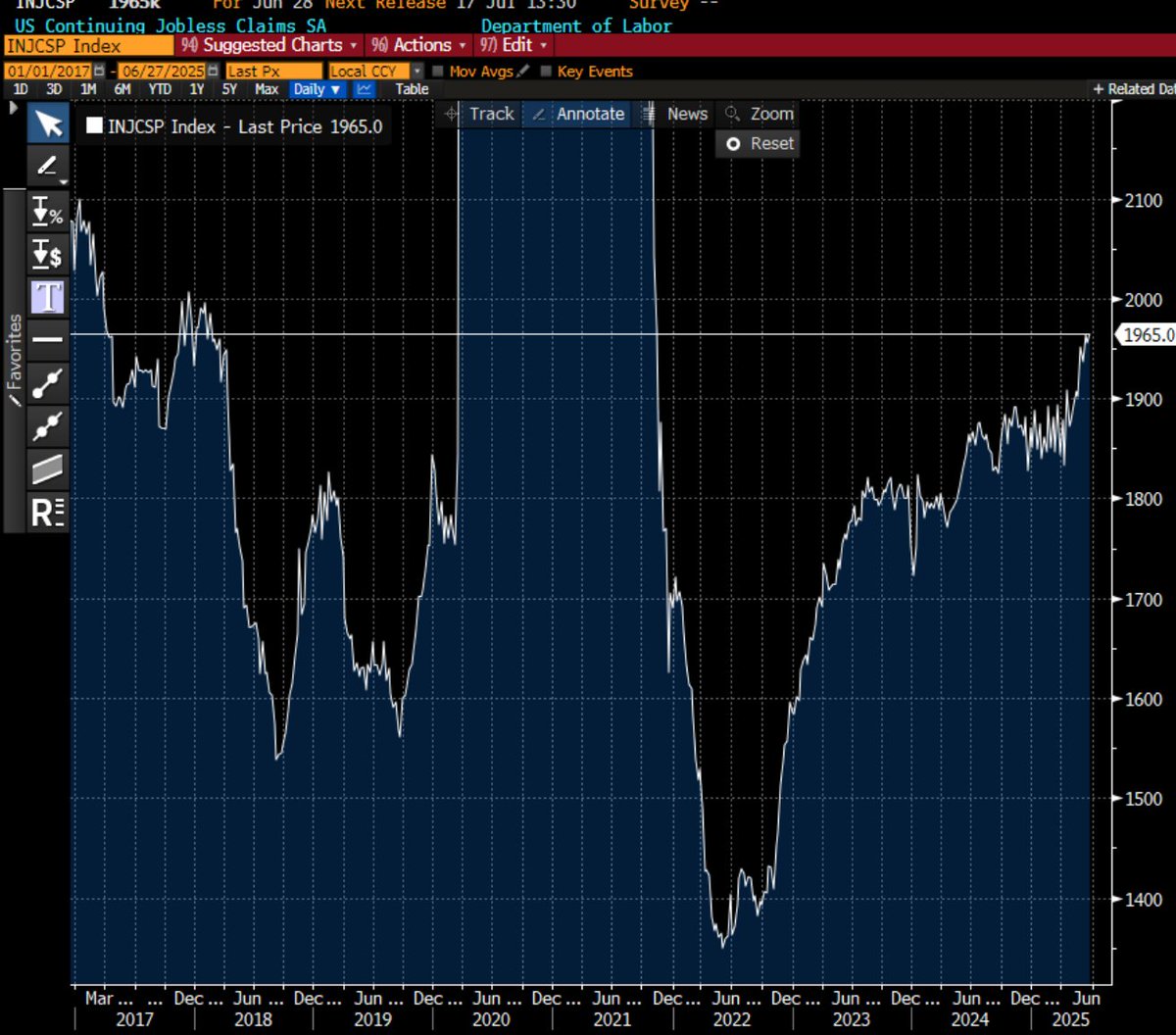

⚠️ US continuing claims hit a fresh post-Covid high at 1965k. Whilst the velocity of layoffs isn't picking up, continuing claims creeping up may imply that it's getting harder to find a job $USD

Disinflationary impulses are less transitory than inflationary ones. Lower for longer rates in Europe & China. $USD weakness has a shelf-life

An important distinction that’s definitely not priced in is that whatever transitory bump in coming US CPI print we get, there is a matching and more lasting disinflationary impulse for the ROW.

Chris Waller's odds of becoming next Fed Chair have jumped from 6.5% to 8% on the back of his call for a July rate cut. He's about to double-down on Bloomberg TV shortly. Probably boosts his odds even more $USD

Markets underestimating how logistically hard it is to fire Powell. First Powell has to bring 2 other FOMC officials back to the boardroom. Then they have to discuss whose fault it is that rates haven’t been cut. Then Trump speaks to his 2 advisors. And then someone gets fired 🤓

“Long-end yields seeing escape velocity” “Bond markets tumble on Finance Minister crying” “Top central bank official at risk of being ousted” Must be EM right. Nope, that’s Japan, UK & US in recent weeks. At this rate G10 & EM desks should merge. Difference is splitting hairs

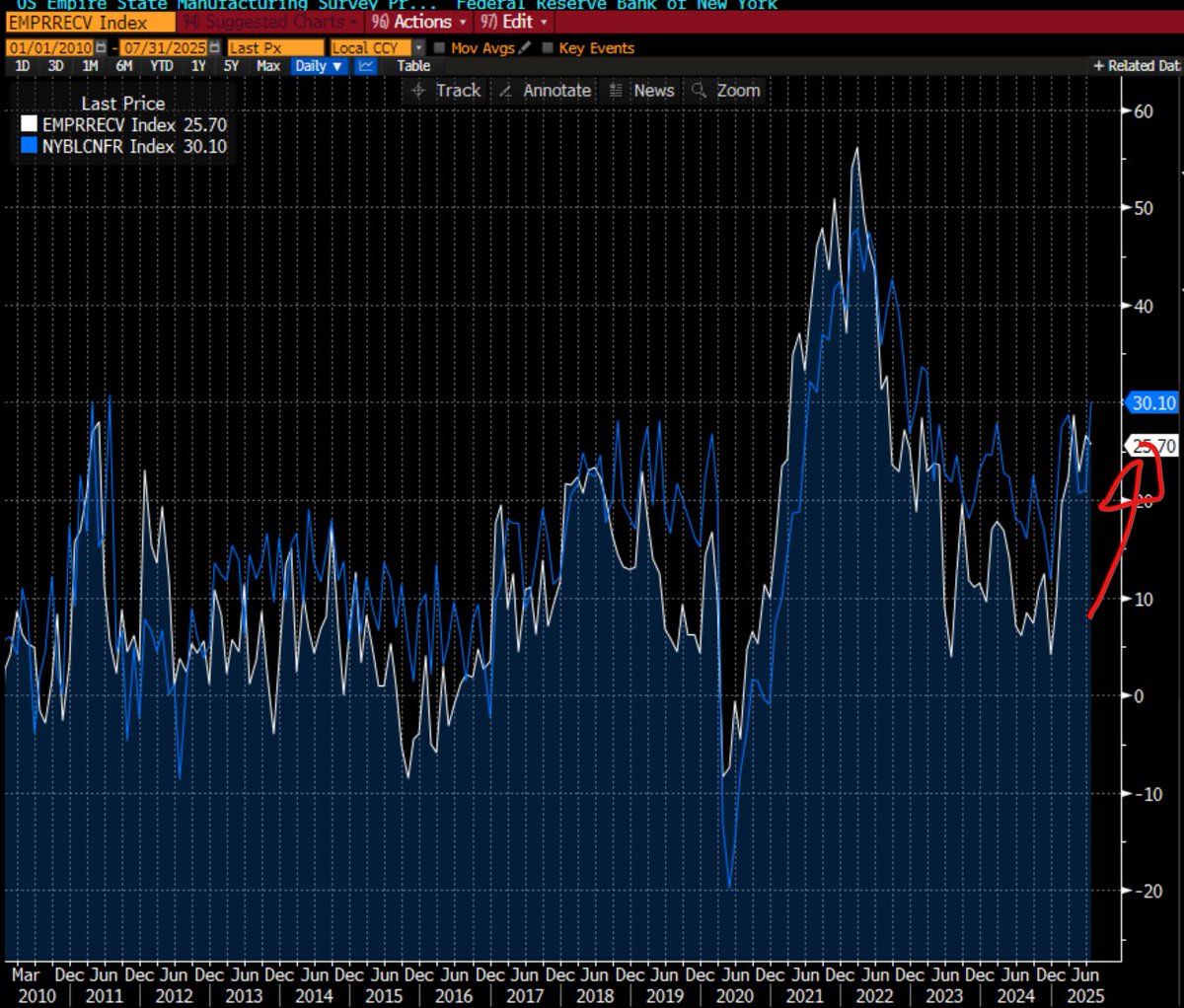

⚠️ If you're worried about inflation, this is your chart: Prices received in the NY Services survey just ticked up to their highest level since March 2023. Increase in manufacturing/goods prices might be spilling over into domestic prices (it's just one month but still) $USD

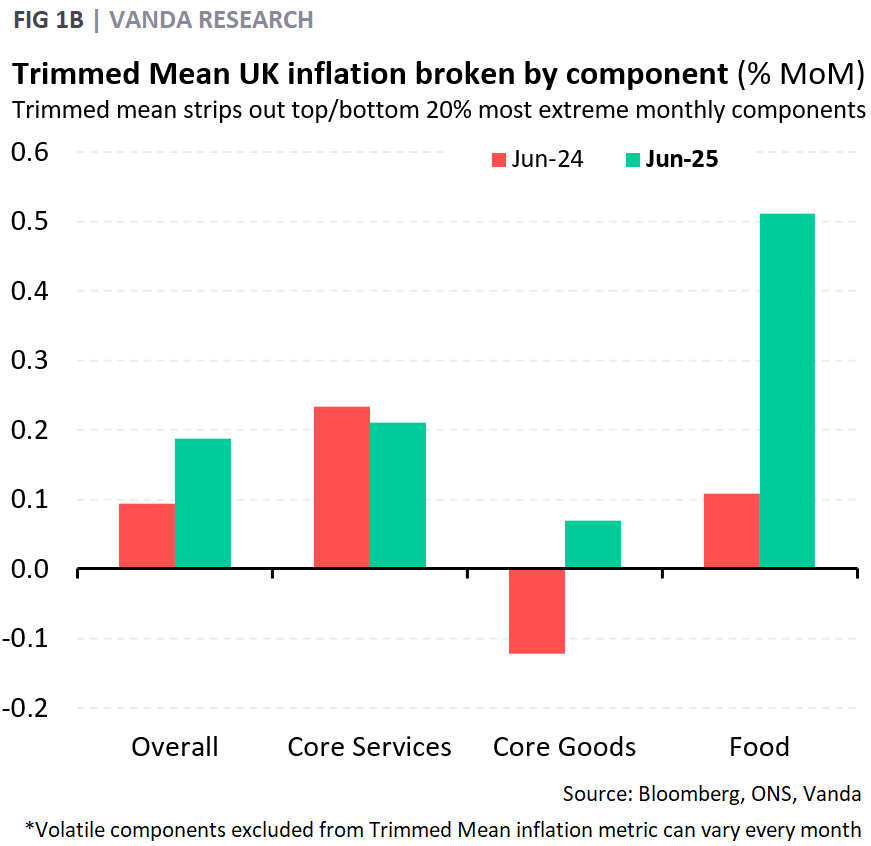

⚠️ Hotter-than-expected UK CPI. But (i) ok breadth (only 46% of basket >2.5% annualised inflation); (ii) ok-ish core services & goods. Food inflation worrying. BoE still on track to cut given weak jobs market. Mkt a bit too excited about front-loaded cuts (slow-burner to 3%) $GBP

Key US data before the Fed cut 50bps last Sep: - 6M annualised core inflation: 2.73% - 6M average private payrolls: 99k Current (Jun-25): - 6M annualised core inflation: 2.68% - 6M average private payrolls: 107k Spot the difference $USD

⚠️ 5th consecutive negative surprise in US core CPI. 4th hottest June since 2001 on an NSA basis. Tariff inflation is showing up a bit. But importantly, inflation isn't picking up as much as markets/Fed feared. Breadth was high. But soft enough for Fed to think about cuts $USD

⚠️ The US labor market *is* cooling. Total job listings on Indeed hit their lowest level since February 2021 (as of July 4) $USD

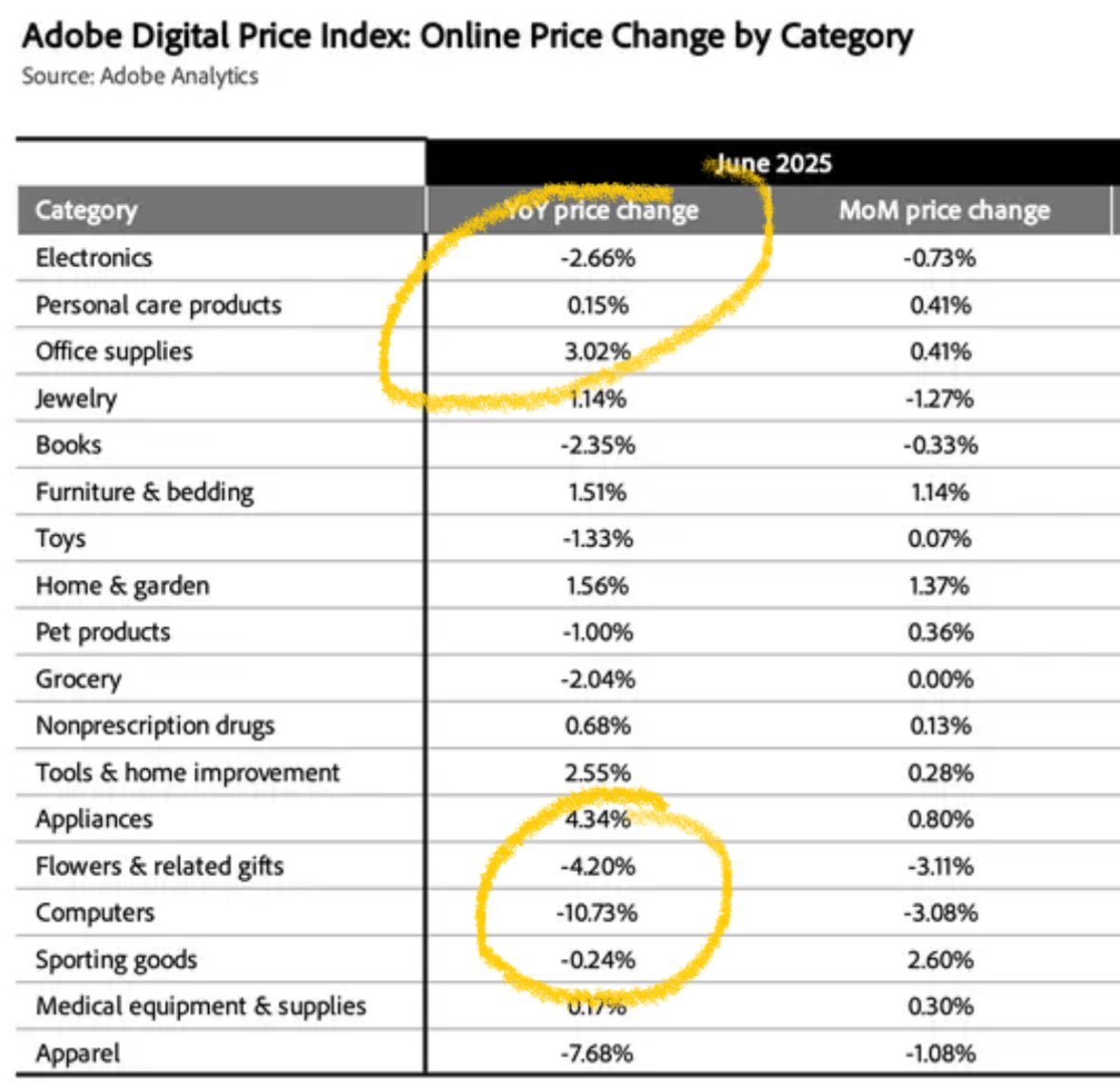

According to Adobe Digital Prices in June 2025… Computer prices down 10.7% YoY, Tous down -1.3% YoY and Electronics down -2.6% YoY. Doesn’t suggest tariffs are all that inflationary so far $USD

If Coach Trump can get Chelsea to win the Club World Cup, then fixing the US trade deficit should be a piece of cake in comparison 🤓

EuroTaxing 🤓 $EUR

I’m very impressed there was: a) someone working in the EU b) on a Sunday c) In July 😳😱😵💫 EU PREPARES RETALIATION AGAINST TRUMP’S 30% TARIFFS

Taiwan exports to US are surging whilst Taiwan imports from Mainland China are surging. Wonder what that means (backdoor channel). Asian exporters in full TACO mode $USD

US administration officially rolling their Reciprocal Tariff future by a month. Next settlement date: Aug 1 Expiration date for deals: Jul 31 Roll period: Last week of July The tariff playbook for the next 4 years (stay on top of the settlement, expiration & roll dates) $USD

BESSENT: THOSE TARIFFS WILL TAKE EFFECT ON AUG. 1