Jeremy

@JeremyWS

EM Macro … FX/Rates/Vol/Credit

After a 7yr hiatus… I’ve finally gotten around to writing some thoughts on the markets whilst travelling about this week… Focused mainly on $ Rates/FX and some glaring disconnects. 2024 looks likes it’s going to be a super interesting year. GL. macrocreditfx.blogspot.com/2024/01/2024-f…

The NBR has sold ~7bn EUR in the past few days (more than 10% of their reserves) trying to slow this EURRON. Much like w Turkey, liquidity is being drained fast and implieds are starting to spike aggressively. 1m to 15% and 1y to 10% still seem achievable. Chart 1month Implieds.

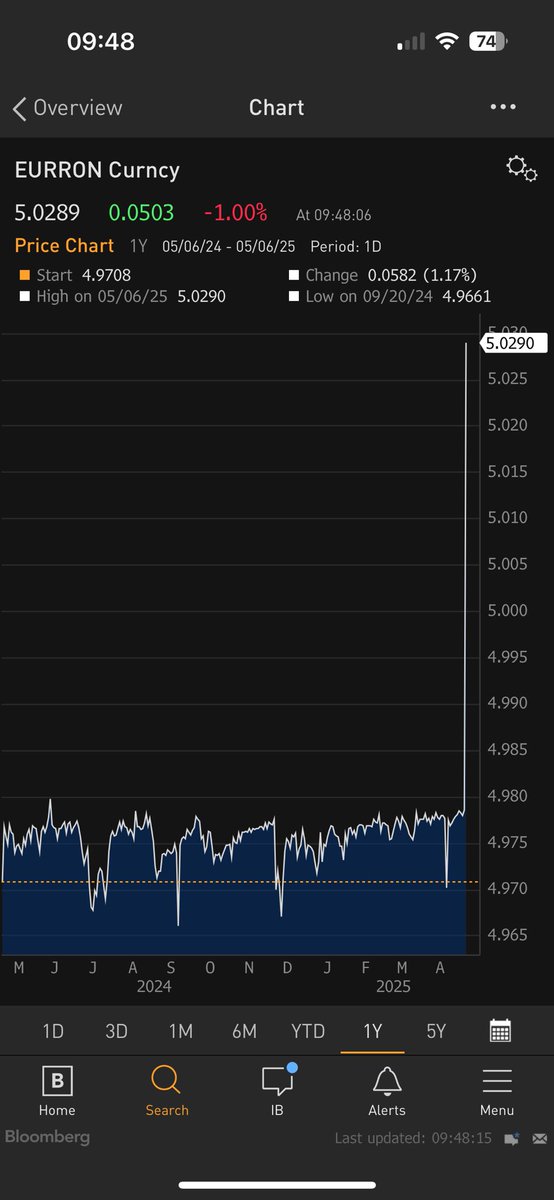

EMFX really popping off these days… now it’s Romanias turns. EURRON breaking through the long held 5.00 level and marching higher fast. Fast money and macro all over this pushing.. let’s see the response.

EMFX really popping off these days… now it’s Romanias turns. EURRON breaking through the long held 5.00 level and marching higher fast. Fast money and macro all over this pushing.. let’s see the response.

Think drift the fix slowly as a soft retaliation this week , up to around 7.25, by end of week.. they then hoping it pressures markets enough to bring sense to trump but idk about that… reprice to 7.75 seems inevitable eventually

CNY fix watching markets are back… looking forward to the 2am wake ups

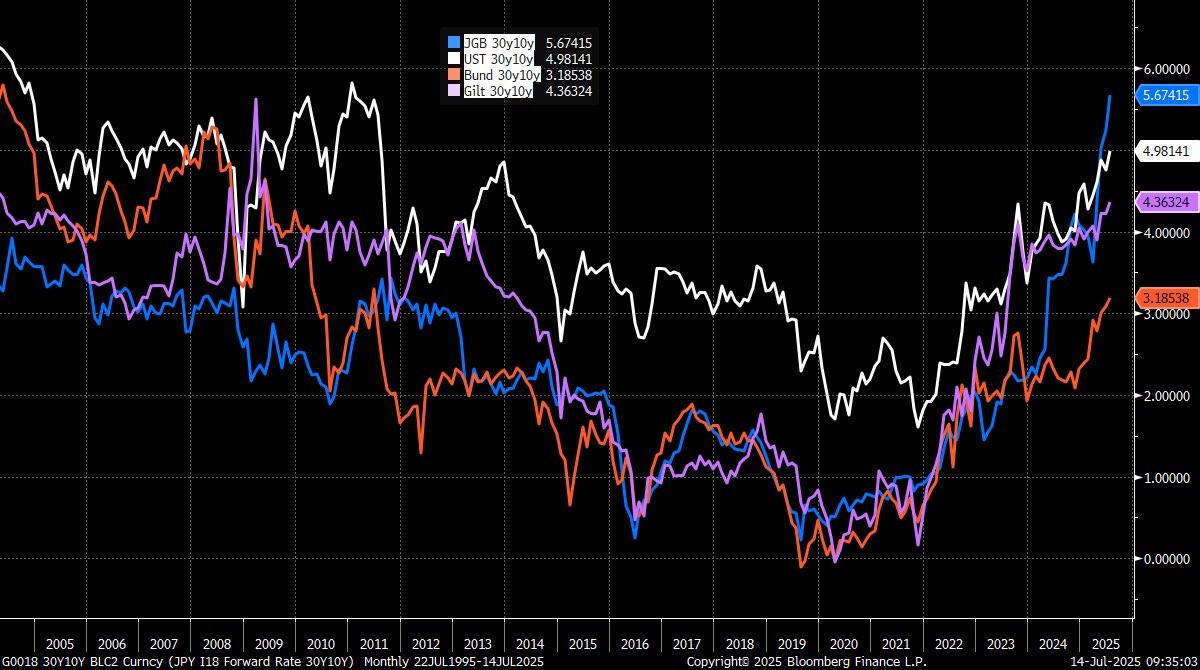

Even more remarkable for JPY rates is the cross market look at ultra long end yields.. this time in cash tho… JGB long end (30y10y) firmly the highest across G4 at 5.7%(!!). Much of it coming from the almost EM level of ASW (220bps) in the back end

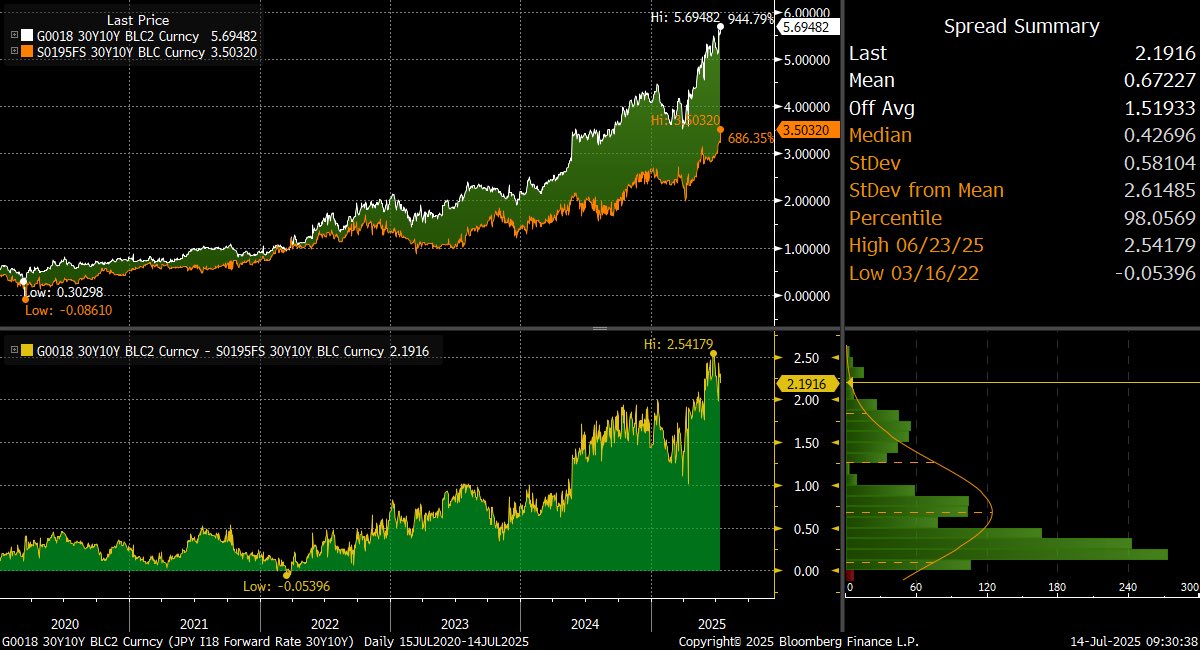

Epic move in JPY rates to start the week. Ultra long fwds (20y10y here) exploding in the bear steepening move.. up 25bps this mng, and 50bps in July. How long till the BoJ realise they will need to hike to help address this disease in the long end?

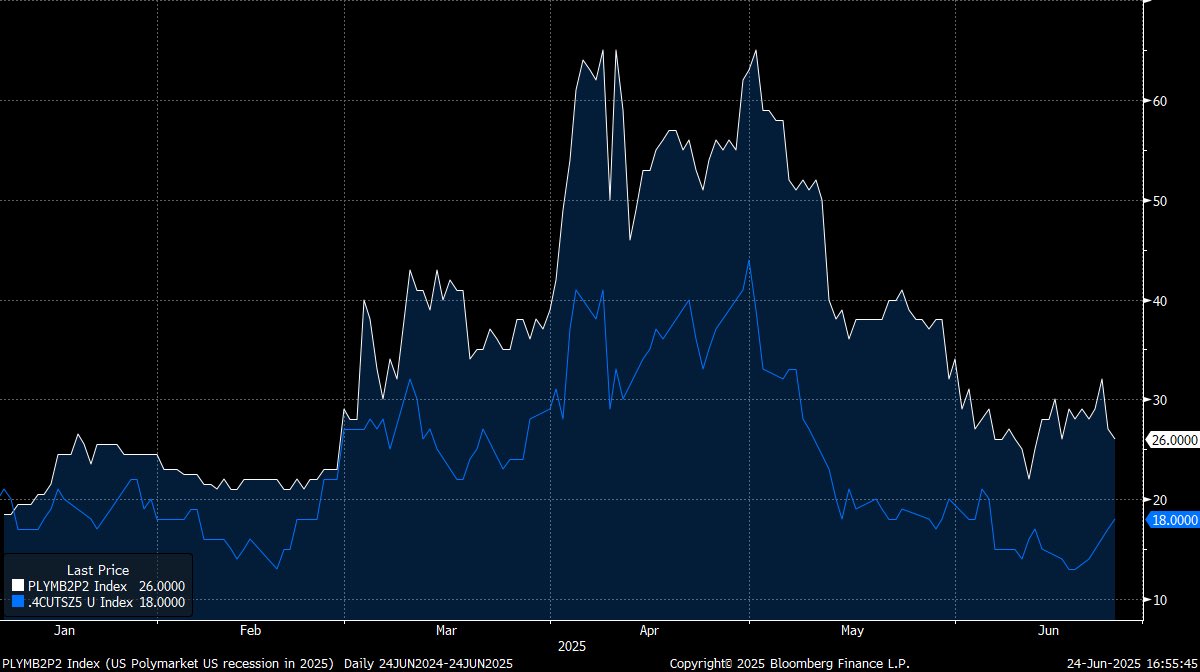

Polymarket odds of recessions Vs SOFR implied probability of 4cuts in 2025 (my rough market implied measure).. notable divergence last few days as the market shifts weight of importance away from labour market/growth and back towards CPI. 15July CPI print gaining event vol.

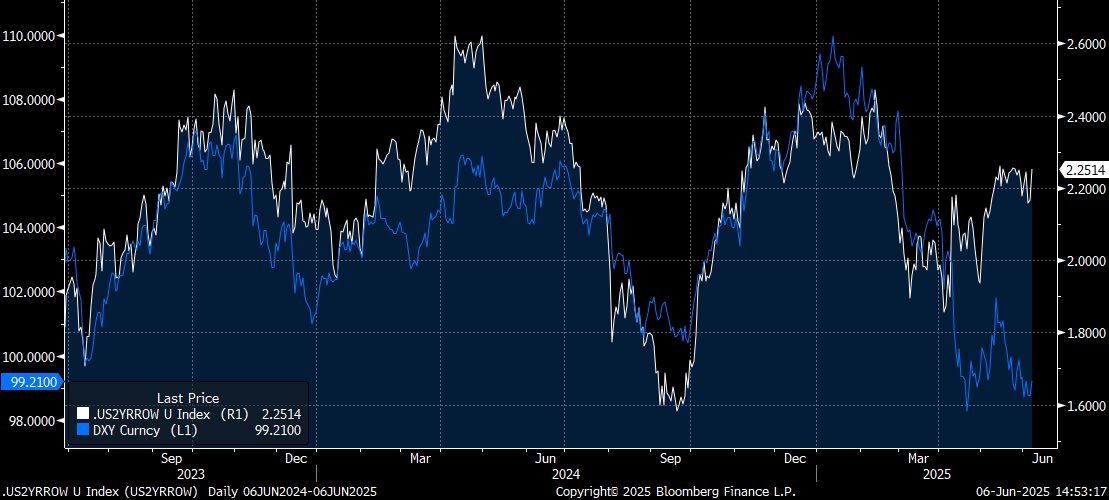

DXY vs 2yr rate differentials… quite literally every soul on the planet is short USD … this won’t end well will it ?

10y Bunds have tried and failed multiple times at the 2.40/50 area… the market has hidden in European FI for the past month as US/JN yields have been volatile… now this positioning is caught offside as we break higher. Still don’t understand why people want bonds, anywhere.

Interestingly various fwd $ rate tenors traded to new cycle wides today (chart 15y10y).. with growth not cracking & fiscal the next story, it doesn’t feel like it’ll be long till we see the same in the spot tenors. 30y UST cycle wides of 5.175 the first stop.

USDHKD forwards are now trading at the biggest “discount” to the bottom of the HKMAs band at 7.75… the last time we traded firmly below was late 2004 as the market prepared for the depegging/free floating of USDCNY from 8.28 in 2005. For the brave , this is free money.

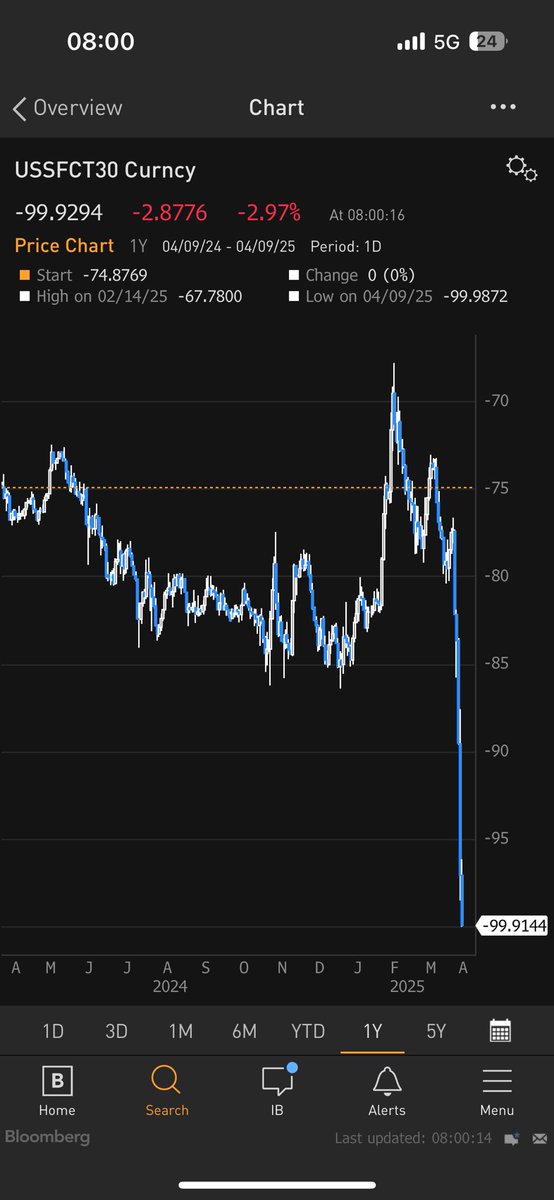

US 30 year swap spread now -100bps.. market really testing the checks and balances in the US (truss like moments)… tho I worry the US won’t find it as easy as the UK to navigate through this … demands for fed cuts won’t help this … how long till the ppl call for QE?

CNY fix watching markets are back… looking forward to the 2am wake ups

With USDTRY spot market functionally frozen, the only tool to chase/hedge is CDS.. trading up at 325 now (post roll). A game of hot potato tho, as not that clean… fx fwds pushing higher again… TKY once again seems trapped with no good options to choose from

USDTRY remembering Erdogan does stupid things when he feels strong… carry:vol metrics have pulled so many into this trade